Analysis of the current housing market and its prospect

In 2014, the real estate market in China experienced a market downturn for the first time due to non-external factors and policy factors, and the investment growth rate continued to fall, with negative growth in many indicators such as housing sales area, newly started area and land purchase area. As the local governments gradually loosened the purchase restriction policy, the central bank relaxed the mortgage policy and cut interest rates, the market showed signs of stabilization, the decline in sales narrowed, and the decline in house prices narrowed slightly for three consecutive months. How the market trend will be in the next few years has attracted the common attention of real estate enterprises, governments, financial institutions and buyers.

However, to make an accurate judgment on the future trend of the market, we must first have a comprehensive, clear and accurate understanding of the current situation of the real estate market. Grasping the status quo requires us to first clarify three basic questions: First, how much is the current stock of urban housing? Second, what is the relationship between supply and demand of new commercial housing, and what changes have taken place in the composition of housing demand? Third, what is the degree of differentiation between different cities, and do you need to take similar policy measures? Based on these basic problems, this paper tries to analyze and predict the future trend of the property market on the basis of studying the current market situation, and puts forward some policy suggestions, hoping to help promote the sustained and healthy development of the housing market.

Analysis of the Current Situation of Housing Market

1. What is the stock of urban housing?

As for the stock of urban housing in China, because the official institutions have not released this data, different scholars have used different methods to measure it, but the measurement results are quite different. Based on the completed area of commercial housing over the years, some people think that the current urban housing stock is only about 15 billion square meters, and the housing supply is still in short supply, so the market will continue to grow rapidly in the future; Some people calculate the completed residential area in the construction industry over the years, and think that the urban housing stock has reached 30 billion square meters. If we consider the small property houses, the housing stock will be even larger, and the real estate market in China has peaked. Others calculate by multiplying the urban per capita housing construction area by the urban population, and think that the housing stock is around 24 billion square meters, and the housing problem has been initially solved.

Personally, these calculation methods and results are debatable. Based on the completed area of commercial housing, only commercial housing is considered, but the factors of non-commercial housing are not considered, so the stock scale of the market will be seriously underestimated. The calculation based on the completed area of the construction industry does not take into account the difference in statistical caliber between housing and urban housing in the construction industry, so it will be overestimated. It seems accurate to calculate the per capita housing area, but there are still some errors in the calculation results because the per capita housing area is based on household sampling survey.

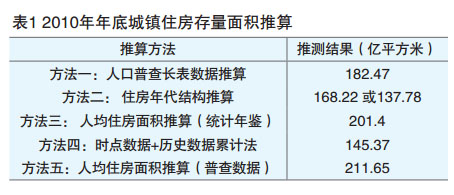

Relatively speaking, we believe that the relevant data of the national census is more accurate, so we can use the relevant data of the sixth census in 2010 (including the age structure of housing, per capita housing area, 10% sampled total housing construction area, etc.) to calculate the stock of urban housing in that year, and then combine the data of the completed area of urban housing over the years since 2011 to calculate the stock data at the end of 2014. In addition, it can also be calculated by using the data of urban housing area in 2005 published by the Ministry of Housing and Urban-Rural Development and combining the data of completed urban housing area over the years. Finally, we can infer a relatively scientific and reasonable housing stock data by comprehensively analyzing the data differences of several different calculation methods. (See Table 1)

As can be seen from Table 1, the estimated urban residential stock area at the end of 2010 has the highest value of about 21.2 billion square meters and the lowest value of about 13.78 billion square meters. It can be inferred that the real stock of urban housing should be between these two values. Further, considering that the per capita housing construction area index is calculated by family households, excluding collective households, the value will be on the high side. Taking all factors into consideration, we believe that the housing stock area of cities and towns in China was about 18.247 billion square meters at the end of 2010. On this basis, we speculate that the stock area of urban housing in China will reach 22.4 billion square meters by the end of 2014.

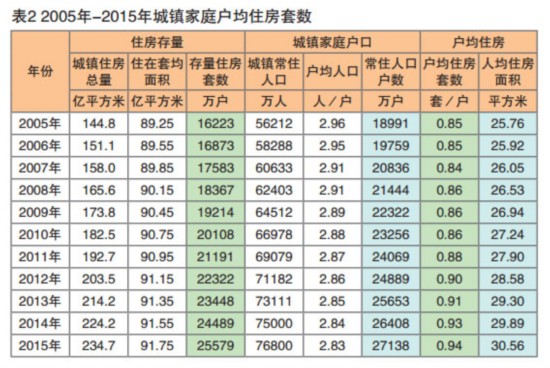

Because everyone feels more abstract about the total area of housing, it will be more intuitive for us to convert it into the number of houses. In 2005, the number of urban housing units in China was 162 million. At that time, the number of households with permanent urban population was 190 million, and the average number of housing units per household was 0.85. In 2014, the stock of urban housing reached 245 million sets, and the number of urban households was 264 million, with an average of 0.93 sets. It is estimated that around 2020, China will achieve the goal of 1 suite per urban household. (See Table 2)

From the perspective of market supply and demand, since the housing system reform, with the gradual release of housing demand, coupled with the advancement of urbanization, urban housing demand is relatively strong, and the contradiction between housing supply and demand is more prominent, especially since 2003, housing prices have continued to rise rapidly.

Since 2010, with the acceleration of the construction of affordable housing, the market supply and demand have eased. However, due to people’s strong expectation of rising house prices, the proportion of investment houses is high, and the market supply and demand are still manifested as virtual heat. In 2011, in order to curb the excessive rise of housing prices, a total of 47 cities across the country began to implement the housing purchase restriction policy, and the demand for investment housing was effectively suppressed. However, the expectation of rising house prices is still strong, and the relationship between supply and demand in the market is still relatively tight. Even in 2013, house prices in first-tier cities such as Beishangguangshen and Shenzhen rose by more than 20%. In 2014, the relationship between supply and demand in the housing market quietly changed. With the tightening of housing credit policy, housing sales suddenly became cold, and the relationship between supply and demand in the market reversed, and there was an obvious oversupply. Many people think that 2014 is an important turning point in China’s real estate market.

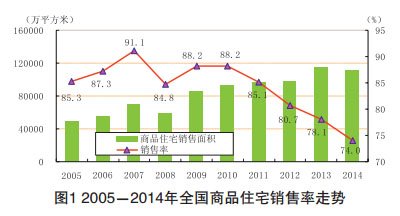

However, through the analysis of relevant data, we find that, in fact, the real turning point of the relationship between supply and demand in the housing market was in 2010-2011. Since 2010, the sales rate of commercial housing has continued to decline. In 2014, the sales rate of commercial housing hit a new low since 2005, only 74%. Moreover, since 2012, the sales rate of commercial housing has been lower than that during the financial crisis in 2008, which shows that the relationship between supply and demand in the market has been quietly changing in 2012, but the housing sales situation at that time was still relatively hot, which did not attract everyone’s attention.

Judging from the total demand for commercial housing, since 2010, except for the high growth rate in 2013, the growth rate of commercial housing sales area in other years has not exceeded 10%, far below the previous growth level. From the perspective of Beijing and Shanghai, the sales area of commercial housing has peaked in 2006 and 2007 respectively, and the sales area in subsequent years has not exceeded this level. The big cities such as Beijing and Shanghai are a microcosm of the current urbanization in China. It is inferred that in the next few years, the sales area of commercial housing in other cities in China will also peak one after another, and the total demand for commercial housing will slowly decline. (See Figure 1)

This can also be seen from the composition of housing demand. The demand for housing mainly includes four parts: first, the demand for buying a house for the first time, which mainly includes two parts, one is the demand for housing brought about by the teenagers in the city’s own population growing up and getting married, and the other is the demand for housing for the newly transferred population in the town in the process of urbanization; Second, improving demand, that is, with the increase of family income and the change of housing conditions, higher requirements are put forward for housing; Third, the demolition demand, that is, the loss of the original housing caused by house demolition or urban renewal and transformation, thus forming the demand for housing; The fourth is investment demand, that is, the demand for buying houses for the purpose of investment preservation. It should be said that the rapid development of China’s real estate market for 15 years is inseparable from the demand-driven in these aspects.

Judging from the development trend in recent years, the composition of housing demand is also undergoing great changes.

First of all, the scale of first-time buyers has risen steadily, but the demand growth is limited. On the one hand, as the process of urbanization enters the middle and late stage, its advancing speed will slow down, and the scale of urban population increase will drop every year, especially the scale of net increase of urban population caused by urbanization will obviously slow down. The National New Urbanization Plan puts more emphasis on people’s urbanization, which will contribute to the increase of housing demand. On the other hand, judging from the demand for wedding rooms, its scale is closely related to the birth population from 1986 to 1990, and this period is the third birth peak in China, with an average annual birth rate of more than 20‰, and the number of newborn babies is as high as more than 24 million per year, exceeding the previous level by more than 3 million. Most of these people have reached the age of work and marriage. Although the number of people buying houses for the first time is on the rise, it will take time for these groups to turn into effective housing demand with the rise of housing prices because of their relatively limited purchasing power.

Secondly, the demand for improved housing has increased significantly. With the improvement of residents’ income level and the increase of the number of households’ housing units, the demand for improving housing conditions of the groups that have bought houses is increasing. The number of people who "sell small and buy big", "sell old and buy new" or buy a second home directly is increasing. It is expected that the scale of future improvement demand will exceed the demand for first-time home purchase and become the main demand of the property market.

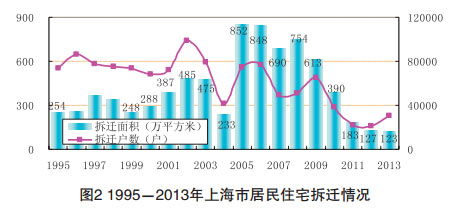

Thirdly, the scale of demolition demand has dropped significantly. According to the data of the sixth population census, at the end of 2010, the proportion of urban housing before 1980 was 5.8%, with a total of 1.17 billion square meters, which is likely to be demolished in the future. However, due to the standardization of demolition and the rising cost, the scale and progress of demolition will slow down. Moreover, more and more families will choose to move back in place or resettle their houses in different places, and their demand for commercial housing will be significantly reduced. As the national demolition data has not been published, we take Shanghai as an example (see Figure 2). From 2005 to 2009, the scale of residential demolition in Shanghai was relatively high, and it dropped significantly after 2010. In 2011-2013, the scale of demolition was even lower than that before 2000. As the epitome of the whole real estate development in China, Shanghai’s development trend also represents the future trend of the national market.

Finally, the demand for investment housing has dropped significantly. There are three main reasons for this: first, the impact of the purchase restriction policy has led to the forced withdrawal of investment demand in some cities; Second, with the rise of internet finance, investment and wealth management channels have increased, attracting some idle social funds to enter; Third, with the promotion of the unified real estate registration system and real estate tax, the whole society’s expectation of future house price decline has increased, and the expected return of real estate investment has declined, which has led to the transfer of this part of funds to other channels. According to relevant surveys, in the past two years, the investment purchase ratio of urban housing has dropped from nearly 20% to about 5%.

It should be noted that the above analysis is about the demand for the whole housing, and commercial housing is only a part of it. Besides, affordable housing, second-hand housing and rental housing are also important ways to meet the housing needs of residents. Judging from the proportion of the completed area of commercial housing in the completed area of urban housing in recent years, it is basically stable at about 73%, which shows that only about 73% of the new housing demand is realized through commercial housing.

3. Differentiation of different cities

The real estate market has strong regional characteristics. When the overall market is adjusted and dropped, different cities will have obvious differentiation.

Judging from the growth rate of the sales area of commercial housing in 35 large and medium-sized cities since 2011, 19 cities experienced negative growth in 2011, 10 in 2012, 6 in 2013 and 29 in the first 11 months of 2014. Differences between different cities have always existed. In the first 11 months of 2014, the sales area of commercial housing in 29 of the 35 key cities declined, while the remaining six cities maintained growth. Among them, housing sales in seven cities, including Beijing, Fuzhou, Changsha, Shenyang, Harbin, Guiyang and Dalian, were sluggish, and the sales area dropped by more than 20%. In sharp contrast, Lanzhou, Yinchuan, Wuhan and other cities increased greatly, especially Lanzhou, where the sales area increased by 99.5%.

For the current differentiation trend of different cities, we should not only see the inevitability, but also consider their differences. For the real estate market adjustment and market oversupply in 2014, different cities can be divided into two situations: one is absolute surplus, that is, the supply of housing absolutely exceeds the actual demand level, even if the market picks up, the relationship between supply and demand is difficult to change quickly; The other is relative surplus, that is, oversupply is only affected by policy restrictions and expectations, and housing demand is greatly suppressed, resulting in temporary and relative oversupply. Once policy restrictions are lifted, market expectations will change, housing demand will be released in large quantities, and the market will resume the state of short supply.

Judging from the comparison between first-and second-tier cities and third-and fourth-tier cities, most of the first-and second-tier cities are relatively surplus at present, such as Beijing, Shanghai and other cities, and their potential demand is still relatively large, but it has not been released for the time being due to the expected impact and limited purchasing power. However, some third-and fourth-tier cities are absolutely surplus, such as Ordos, Yingkou, Changzhou and Yulin. The housing supply in these cities has seriously exceeded their affordability, and "ghost towns" and "empty cities" are typical manifestations. Judging from the reaction of cities since the central bank relaxed the mortgage policy and cut interest rates in the second half of 2014, the rise in first-tier cities and some second-tier cities is more obvious. According to the contracted area data of commercial housing in key cities in the fourth quarter, the growth rate of Beijing, Tianjin, Guangzhou, Shenzhen, Nanjing, Changsha, Nanning and other cities all exceeded 50% month-on-month, and the rebound trend was more obvious. The growth rate of Shanghai, Hangzhou, Xiamen, Wuhan, Chengdu and other cities also exceeded 20% month-on-month.

Reasons for this round of adjustment in housing market

For the adjustment of the housing market in 2014, some people think that the tightening of credit policy is the main reason. In fact, the tightening of credit policy is only a fuse, and there are many reasons behind the market adjustment. Among them, there are factors such as the continuous rise of housing prices, overdraft purchasing power, macroeconomic adjustment and changes in population structure, as well as factors that lead to the exit of investment housing.

On the whole, there are four main points: first, the age structure of the population changes and the growth rate of new urban population slows down, and the demand for first-time home purchases slows down; Second, rising housing prices have led to a decline in residents’ actual purchasing power and an increase in the real estate bubble; Third, the purchase restriction policy has caused some investment houses to be squeezed out, and the expected decline in future housing prices has delayed some housing demand; Fourth, the "substitution effect" of affordable housing and second-hand housing on new housing has increased, which has led to a further decline in the demand for new commercial housing.

1. Demographic factors lead to the overall slowdown in the demand for first-time home purchases.

Judging from relevant theories and international experience, the trend of population change determines the long-term prosperity and depression of the real estate market to some extent. This trend includes two aspects, one is the change trend of the total population, that is, whether the total population is increasing or decreasing, the change of the growth rate of the total population, etc., and the other is the change trend of the structure, that is, the urban and rural structure, age structure and regional structure of the population.

Judging from the trend of total population, China’s population size is on the rise. However, judging from the changing trend of the total population, its average annual growth rate will show a low growth trend. Since 2009, the natural growth rate of China’s total population has been below 5‰ for five consecutive years, with the lowest value of 4.79‰ in 2010-2011. Since 2012, with the adjustment of China’s family planning policy, the natural population growth rate has slightly increased, but the overall level is still at a low level.

Judging from the trend of the total urban population, it is predicted that with the steady advancement of urbanization, the urban population scale will continue to grow in the next 10 years at least, but the growth rate will slow down. We divide the urbanization process from 1996 to 2013 into three periods: 1996-2003, 2004-2010 and 2011-2013. It can be found that the average annual growth rate of urbanization in these three periods was 1.44, 1.35 and 1.26 percentage points respectively, and the growth rate showed a downward trend. It is estimated that the proportion of urban population in China will increase to about 60% in 2020. Based on this calculation, it is estimated that the urbanization rate will increase by about 0.9-1 percentage point every year from 2014 to 2020. In a word, it is expected that the speed of urbanization in China will slow down slightly in the future. As a result, the total housing demand caused by the increase of urban population will fall back, but its total amount is still considerable.

From the structural point of view, it can be analyzed from the age structure and regional structure of the population. From the age structure of population, the proportion of economically active population in China shows a downward trend. 2011 is a turning point in China’s population structure. In that year, the total dependency ratio of the whole society (including the dependency ratio of children and the dependency ratio of the elderly) increased. This is the first time since the reform and opening up, which indicates that the "demographic dividend" factor supporting the miracle of China’s economic growth for 30 years tends to disappear. Correspondingly, the proportion of economically active population in the whole society also declined in that year, and this downward trend will continue in the future. What is even more worrying is that with the acceleration of aging, it is predicted that in the next three years, the absolute number of the economically active population in China will decline on the basis of the decline in the proportion. The economically active population is the main body of housing consumption. With the decrease of the economically active population, the corresponding housing consumption demand will also fall back.

Judging from the regional population structure, there is obvious differentiation among different provinces. According to the changing trend of the total population in different regions from 2002 to 2013, the total population in five provinces and cities showed an absolute decline, including Guizhou, Henan, Anhui, Guangxi and Sichuan. The total population of other provinces and cities maintained growth, among which Guangdong, Zhejiang, Shanghai, Beijing, Shandong, Hebei and other economically developed areas grew rapidly. Judging from the trend of population changes in the future, this feature will continue.

In short, in terms of the total population, the population growth rate will slow down in the future. From the perspective of population structure, the proportion of economically active population has decreased, the proportion of elderly population has increased, and the population flow between regions has accelerated. Affected by it, the scale and price increase of real estate transactions will slow down or even fall in the future, and the market differentiation between different cities will intensify.

2. Excessive housing prices lead to a decline in residents’ purchasing power.

Since 2009, China’s housing prices have once again entered a period of rapid rise. Judging from the national average house price, it increased from 3,800 yuan in 2008 to 6,237 yuan by the end of 2013, with a cumulative increase of 64.1% and an average annual increase of 10.4%. If we consider that this price is only the average selling price, and if we consider the trend that housing development is far away from the central city, the actual increase in housing prices will be even higher. With the continuous rise of housing prices, the real estate bubble is increasing. On the other hand, due to the expectation of rising house prices, people are forced to spend ahead of schedule, and some demand is overdrawn in advance. Although this has caused the current real estate market to continue to be hot, it will lead to the shrinking demand for housing consumption in the later period, which has caused great hidden dangers for its later adjustment.

From the international experience, two indicators are mainly used to measure the degree of real estate bubble in a country or region. One is the ratio of house price to income, that is, the ratio of the overall level of house price to the income of households. The second is the ratio of housing rental to sales, that is, the ratio of housing sales price to rent.

Judging from the ratio of house price to income, it is generally maintained at three to six times as a reference internationally. However, due to the differences in the source and selection of data, the definition of calculation indicators and cultural factors, the dispersion degree of house price-income ratio in different countries is quite large, and it is of little significance to compare the house price-income ratio only internationally. However, for the same area, the changes in different years can dynamically measure the local residents’ ability to buy houses and the level of housing prices.

On this basis, we have calculated the value of the ratio of house price to income since the reform of the housing system in China (see Table 3). The results show that the ratio of house price to income in China has shown an upward trend in the first half of the housing system reform, while it has shown a downward trend in the second half of the housing system reform. The data shows that in recent years, the income of households can buy more houses, which also shows that the house price is more reasonable. However, the fact is not so simple, because when calculating the ratio of house price to income, we use the average selling price of commercial housing in China instead of the homogeneous price. However, judging from the characteristics of real estate development in recent years, it basically belongs to the development mode of "spreading cakes", that is, giving priority to the development of lots with better geographical location, and then developing lots with inferior regional location. Therefore, the income from house prices is actually low. If this factor is taken into account, the degree of decline in the ratio of house price to income in China in recent years is not obvious.

Judging from the data of rent-to-sale ratio, due to the lack of overall national rent data, we take Beijing, Shanghai, Guangzhou, Wuhan, Shenyang, Chengdu and other cities as representatives to measure. The results show that there are great differences among different cities. Among them, the rental/sales ratio of commercial housing in Beijing is the highest, and the rental/sales ratio in the central area even exceeds 1: 800, and the rental/sales ratio in the sub-central area also exceeds 1: 500. The rental/sales ratio of Wuhan, Shenyang, Chengdu and other cities is relatively stable, keeping within 1: 400. From the international experience, the real estate in a region is running well, and its rent-to-sale ratio should be kept between 1: 200 and 1: 300. If the rent-to-sale ratio is higher than 1: 300, it means that the investment value of real estate is relatively small, and the real estate bubble has already appeared. Judging from the value of the ratio of house price to income in these cities, most of them are obviously higher than the normal level, especially in first-tier cities such as Beijing, Shanghai and Guangzhou.

The above data show that with the continuous rise of housing prices, the degree of real estate bubble is also increasing, especially in first-tier cities, where the degree of bubble is higher. Without considering the rise of house prices, the income of real estate investment is lower than that of other investment channels.

3. Affected by the expected decline in policies and prices, investment demand has withdrawn.

In 2009, under the guidance of the national stimulus policy, the national real estate market rebounded rapidly. In that year, the average price of commercial housing rose by 24.7%, the highest increase since the housing system reform. In order to curb the excessive rise in housing prices, the government has imposed restrictions on purchases in cities where housing prices have risen too fast, and a large number of investment housing demand has been forced to withdraw from the market. In addition, the research and levy of real estate tax will greatly increase the cost of non-owner-occupied housing and have a strong crowding-out effect on the demand for investment housing.

A remarkable feature of investment housing demand is its high elasticity and easy to be disturbed by external factors. Under the combined influence of policy restrictions and the expectation of future house price decline, the demand for investment house purchase has been effectively suppressed. According to relevant surveys, the proportion of investment houses has dropped sharply in the past two years, from 18% at the end of 2009 to about 5% at present.

4. The substitution effect of affordable housing and second-hand housing on new housing is enhanced.

It can not be ignored that commercial housing is only a way for urban residents to meet their own housing needs. In addition, there are the following ways: buying affordable housing or second-hand housing, renting housing and so on.

From the perspective of second-hand housing, with the continuous increase of urban housing stock, the scale of second-hand housing transactions is expanding day by day, and second-hand housing has become an important object of residential housing consumption. According to the analysis of relevant data, in some economically developed cities, the transaction area of stock houses is basically the same as the sales area of new houses, and even the transaction area of stock houses in some cities exceeds that of new houses, which will reduce their demand for new houses. Taking Beijing, Tianjin, Shenzhen, Nanjing, Hangzhou, Xiamen, Wuhan, Chengdu and other cities as examples, the transaction area of second-hand housing in Beijing and Shenzhen has exceeded that of new housing; The transaction area of second-hand housing in Nanjing, Xiamen, Tianjin, Chengdu and other cities has reached more than half of the transaction area of new housing.

From the perspective of affordable housing, since 2009, the investment and construction scale of China’s housing security has increased significantly, and the proportion of affordable housing in commercial housing has also increased significantly. Affordable housing has also formed competition for commercial housing. It can be seen from the relevant data that in 2009-2015, the ratio of newly started affordable housing to newly started commercial housing will reach 52.5%, accounting for about 30% in converted area. Affordable housing has a great drainage effect on the demand of commercial housing with its relatively low price. (See Table 4)

With the increasing activity of second-hand housing transactions and the acceleration of the construction of affordable housing, the substitution of the two for new commercial housing is becoming more and more obvious. A considerable part of housing demand has been drained to such houses, and the proportion of meeting housing demand through new housing has declined.

In short, the overall decline of the real estate market in 2014 was due to the combined effects of demographic changes, the decline of residents’ ability to buy houses, the withdrawal of investment demand for buying houses, and the drainage of second-hand houses and affordable housing, which led to the change of supply and demand and the spontaneous adjustment of the market.

Prospect of future market trend and policy suggestions

We might as well describe the housing market situation in recent years with seasons. It can be said that 2009-2010 was like a hot summer, with hot investment and sales, and the house price rose rapidly. In 2011-2013, as in the late summer and early autumn, the purchase restriction policy and the acceleration of the construction of affordable housing made the whole market feel a little cold, but the power of the "autumn tiger" remained undiminished, the market maintained a strong momentum of progress, and even individual cities could hit new highs repeatedly; In 2014, the market has gradually entered a cold winter, with house prices falling year-on-year, and the market sales situation is sluggish. Although the introduction of a series of stimulating policies, such as relaxation of purchase restrictions, relaxation of loan restrictions and interest rate cuts, slowed down the pace of decline, the overall trend of market decline has not fundamentally changed.

For the real estate market in the next few years, we believe that the market will usher in spring and the overall situation will be better than that in 2014, provided that the policy remains moderately loose. However, under the background of increasing housing stock scale, obvious housing price bubble, slowing down the total demand and increasing the area for sale, the sales pressure in the market is still relatively large, the differentiation among cities is intensified, and the housing price keeps a slight fluctuation and the growth rate slows down.

In the down cycle of the market, with the intensification of market differentiation in different cities, the difficulty of real estate regulation is also increasing. On the one hand, the housing price level is too high, out of touch with residents’ income, and the bubble risk is increasing. The government needs to control the bubble level in order to maintain the long-term healthy development of the market. On the other hand, the housing inventory remains high, and the pressure of "destocking" in the whole market is enormous. The government needs to introduce policies to stimulate demand and accelerate "destocking".

How to achieve the goal of "destocking" without excessively increasing the real estate bubble is a difficult problem. The author believes that the smooth release of self-occupied housing demand will be the key to solve this problem. On the one hand, the demand for self-occupied housing belongs to the real housing demand, which basically will not excessively increase the market bubble; On the other hand, the overall demand for self-occupied housing in China is still relatively high. If we can speed up the release of this part of demand through policies, the problem of high inventory level will be solved to a great extent. Specifically, there are four suggestions:

1. The real estate industry still needs to pay attention to "defoaming" while "destocking".

It is predicted that the risks of China’s housing market will mainly focus on two aspects in the future: first, the risk of housing surplus in some third-tier cities; The second is the risk of housing price bubble in first-and second-tier cities. In view of these two different risks, different policy measures are needed. For the former, the government and enterprises need to find ways to "destock" to achieve stable market development; For the latter, we should not only see the pressure of housing inventory in the short term, but also the government should try to reduce the inventory level. At the same time, because the housing prices in these cities are already on the high side, we must pay attention to controlling the increase of housing prices and avoid the housing price bubble from being enlarged again.

As for the relationship between "destocking" and "defoaming", the author believes that destocking should be a short-term policy measure for the current increase of real estate inventory, while defoaming is a long-term policy orientation. In the process of destocking, we should pay attention not to excessively increase the bubble of real estate, especially in first-tier cities.

2. Increase support for self-occupied housing demand and stabilize the total demand.

The demand for self-occupied housing is the cornerstone of the sustained and healthy development of the housing market. The demand for self-occupied housing mainly includes two parts: one is the demand for first-time purchase, the other is the demand for improved housing, or the demand for second-time purchase. In order to promote the stable development of the market without increasing the bubble level of housing prices, self-occupied housing is the key support object.

According to the current housing stock speculation, it is predicted that in 2020, China will achieve 1 suite per household for urban residents, and the demand for first-time housing, especially for new commercial housing, will drop significantly, while the demand for improved housing will increase. Whether the demand for improved houses can be active will be the key factor to determine the housing market situation in the next few years. However, from the current policy environment related to improved houses, it is not conducive to the release of the demand for improved houses. It is suggested that the existing relevant policies should be adjusted, and the first improved home purchase with per capita housing area lower than the local average level should be regarded as the first home purchase, enjoying the same policy conditions and encouraging residents to release the demand for improved home purchase.

Specifically, there are three main points:

First, the transaction process is facilitated. For some improved property buyers, they usually adopt the way of "selling small and buying big" or "selling old and buying new", and the sale of housing always has a process, and it takes some time to buy or sell. According to the current relevant policies, there will be obvious differences in related taxes and fees, including personal income tax, deed tax, loan interest rate and so on. From a practical point of view, there is no essential difference between selling before buying and buying before selling. It is suggested that families should enjoy the same policy treatment as "selling before buying" in a certain period of time, so as to reduce transaction costs and promote market transactions.

Second, the deed tax collection is equal. In the deed tax policy, if you buy the first ordinary house, you will enjoy preferential policies, but if you buy the second house, you will not enjoy preferential policies. In order to enliven the market and promote "destocking", it is suggested to enjoy the same preferential deed tax policy as the first suite for improved houses with per capita housing area lower than the local average.

Third, the loan conditions are similar. In terms of credit policy, with the central bank’s re-identification of the first home loan standard, as long as there is no loan under its name, it can lend according to the first home loan standard and enjoy preferential policies, and the credit policy environment for improved home purchase has improved. However, the adjustment of provident fund loans has been delayed. In most cities, the provident fund loans still implement the standard of "recognizing the house and recognizing the loan", and only 30% of the loans meet the conditions of improved house purchase, which is difficult to meet the needs of improved house buyers for low-cost funds. It is suggested that provident fund loans should be recognized by the same or similar standards as commercial loans, and the release of improved houses should be encouraged.

3. Continue to maintain moderate restrictions on the demand for investment housing, and first-tier cities continue to implement the purchase restriction policy.

For the demand for investment housing, its main purpose is to gain income from rising housing prices. If this part is too high, it will affect the stable and healthy development of the market. Therefore, for investment housing, we should also impose moderate restrictions. For first-tier cities with relatively concentrated population, because of their relatively concentrated resources in all aspects, large foreign population and strong housing demand, the pressure of rising house prices is relatively great. Therefore, policy adjustment in these cities needs to be more cautious to avoid excessive policies leading to a large increase in investment demand, which in turn leads to retaliatory rebound in house prices.

For the purchase restriction policies in first-tier cities, we can fine-tune them according to the local actual situation, such as relaxing the years of paying social security, and expanding the size of the groups that can buy houses. However, it is not appropriate to completely cancel the purchase restriction, because it is likely to lead the market to reproduce the situation of soaring housing prices in 2009 and increase the risk of bubbles. At the same time, because the market trend of first-tier cities has a strong demonstration effect on the national market, once the housing prices in first-tier cities get out of control, the national housing prices are likely to rise again in an all-round way, and the staged achievements of real estate regulation in previous years will also fall short.

4. Stabilize housing price expectations and promote the healthy development of the real estate market.

Because housing has the properties of both consumer goods and investment goods, and its asset value is still relatively high, the future price trend is expected to have a huge impact on the release of demand. "Buy up and don’t buy down" is a typical manifestation of this psychology. During the downturn of the market, people always hope that house prices can be lowered a little before buying, resulting in a downturn in market transactions. If we want to completely change the market downturn, we must stabilize people’s expectations of future housing price trends.

With the active and steady promotion of the unified registration system of real estate, the expectation of levying real estate tax will become stronger and stronger. It is generally expected that the levy of real estate tax will obviously increase the holding cost of housing, which will lead to the decline of housing prices. However, the extent to which the levy of real estate tax will affect the trend of housing prices depends on many factors such as the scope of real estate tax collection and tax rate. It is suggested that the real estate tax collection plan be announced as soon as possible after it is clear, so as to stabilize residents’ house price expectations and promote the market turnover to return to normal level.

In short, in view of the current market adjustment and the growing area of housing for sale, we should see that the potential housing demand is still relatively strong, and the risk of housing price bubble in some cities is also relatively high, so the government must not only "destock" but also pay attention to "de-bubble". On the one hand, the government should stabilize the housing price expectation, maintain the steady growth and orderly release of demand, and avoid the excessive decline of the market by increasing the support for the first-time purchase and improved purchase; On the other hand, the government still needs to carry out the idea of "de-bubble" in the previous two years, broaden the investment channels of the whole society, moderately curb the scale of investment housing demand, and avoid excessive concentration of funds in real estate, thus increasing the risk of bubble. As a real estate development enterprise, we should also clearly understand the situation, accurately understand the actual level of the future housing demand growth rate, take "destocking" as our core task, set reasonable prices, and promote the sustained and healthy development of the housing market and even the real estate industry. (This article only represents the author’s personal views)